Rental properties are one of the best ways to generate income, but they can also be surprisingly costly to maintain. Many new owners underestimate how much they’ll spend to keep their property in good renting condition.

If you’re thinking about investing in a rental property, it’s critical to understand exactly what you’re getting into. This article will cover some of the most important costs that people don’t take into account when purchasing a rental home.

Rental Home Management

Some people think they can manage their own properties, but this is a good option only for those with significant experience or knowledge in the area. Property management is a time-consuming process, especially if you get to the point where you own more than one property.

Property managers keep things running smoothly by listing your space, identifying tenants, gathering rent payments, overseeing the maintenance of your properties, and more. Without a property manager, you’ll be on the hook for these responsibilities whenever they come up. It’s extremely difficult to manage properties while working another job.

Different managers charge different rates, but you should expect to give up roughly ten percent of the rent for each property they manage. Remember to factor this loss into your calculations when budgeting for a new property unless you have enough time and expertise to handle management asks yourself.

Insurance and Taxes

Insurance and taxes aren’t included in the sticker price of a new property, but they’re often one of the most costly expenses. Keep in mind that you’ll pay different taxes on a rental property compared to what you owe for your primary residence.

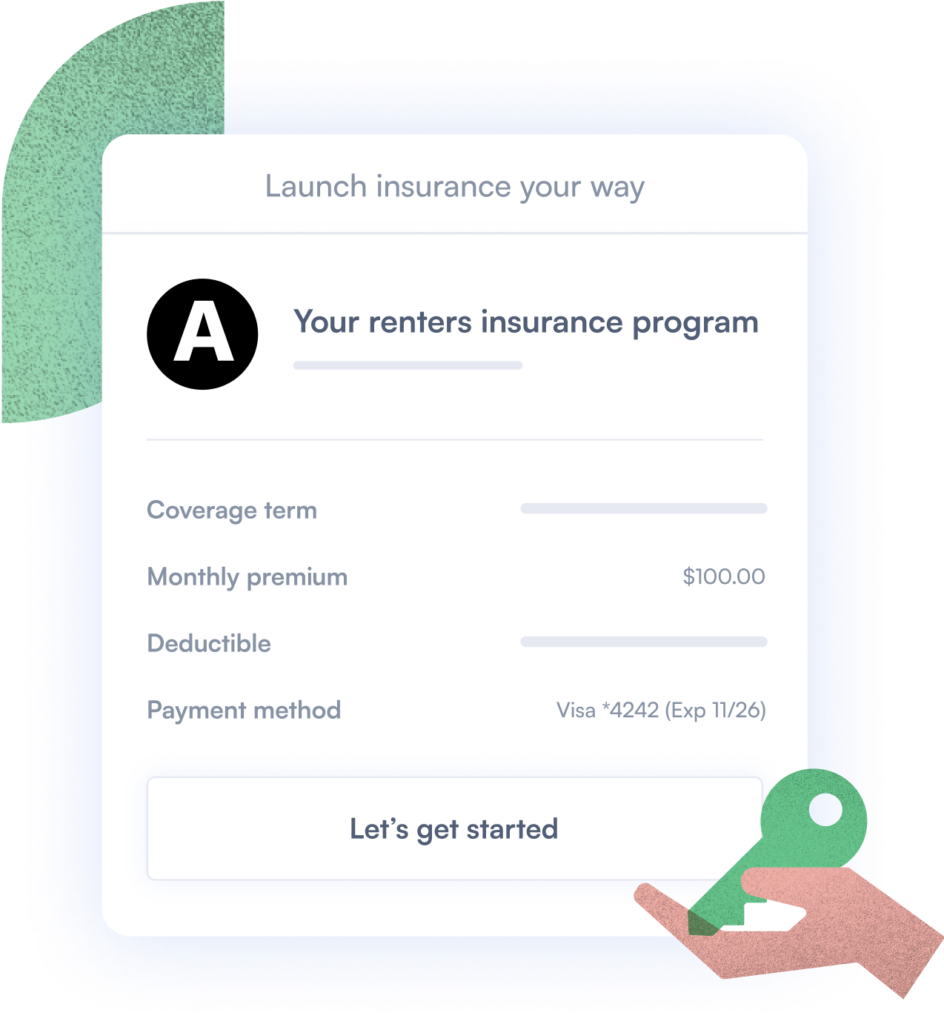

Similarly, rental property insurance is typically more expensive than policies that cover only a residential property. These additional costs protect you from risks that aren’t involved with a primary residence including lawsuits filed by your tenants. You’ll need to get landlord liability insurance to make sure you’re fully covered.

In general, landlord insurance costs about fifteen to twenty percent more than conventional homeowners insurance. Of course, your premiums will also depend on the property itself along with your perceived level of risk. Shop around with a few different landlord insurance providers to look for the right policy for you and your property.

In addition, make sure to encourage that your tenants take out a renters insurance policy for themselves.

Upkeep

Every landlord hopes their property stays in perfect condition, but the reality is that things can be damaged or broken anytime. This is an especially important risk to consider if you own an older property with outdated features. You should try to save at least one percent of the property’s total value every year, or more if it’s at a higher risk of damage.

As with property management, how you deal with maintenance issues is entirely up to you. Landlords with more time may prefer to address problems themselves to save money. On the other hand, it’s hard to achieve reliable results if you don’t have significant handyman experience. Low-quality DIY jobs will end up costing you much more than paying for a qualified professional.

At Latchel, 30% of the maintenance requests that come in from tenants are solved over the phone via troubleshooting. For a step by step comprehensive guide on how to troubleshoot your maintenance costs down, you can download Latchel’s e-book here.

With that in mind, you should expect to have to spend some money on a property manager, or maintenance service provider like Latchel, along with contractors for various issues. These are smart investments for the majority of landlords who don’t have the time, money, or expertise to handle these tasks themselves. You should only try to take these on yourself if you’re very confident in your abilities.

Repair or Replace?

Each landlord has a different approach to upkeep depending on their preferences. Some people try to repair older items for as long as they can get them to last. This helps you avoid investing in a brand-new product for as long as possible. On the other hand, minor repairs add up over time and can easily cost more than a one-time replacement.

If an appliance is more than halfway through its total lifespan and has a history of unreliability, you should consider replacing it rather than stringing it along with repairs—especially if the cost of repairs is close to the cost of a replacement. On the other hand, repairing is usually the best option if it’s a relatively affordable job and you expect to get several more years out of the product.

Vacancy

You can use rent money to fund these costs when a property is occupied, but you won’t have any income to draw on during periods of vacancy. Minimizing vacancies will help you manage your expenses without having to pay for them out of pocket. That said, there’s no way to completely eliminate the risk of vacancy.

Setting your rent too high will drive away potential tenants and leave your property on the market for longer. Going too low will reduce your income and impact your ability to afford costs related to the property. Balancing the advantage of higher rent payments with the benefits of finding a tenant quickly is one of the most important challenges for property owners.

The optimal rent depends on a wide range of factors, but landlords often ask for one percent of the property’s value per month. If you just paid $150,000 for a new property, for example, you should consider charging around $1,500 per month in rent. Check listings in your area to get a better idea of how much you should ask for.

You can also reduce the impact of a rental vacancy by setting up an account to temporarily cover costs. Even just a few months’ worth of expenses can be enough to get you through a difficult period without having to take money out of your own accounts. Contribute a small amount of each rent payment toward your emergency fund, even if you’ve already reached your goal—it’s impossible to predict how long your property could end up vacant and how much it could cost you.

Rental properties are a great investment, but these and other hidden costs can cut into your income and make it harder to generate positive returns. Keep these expenses in mind if you’re thinking about a new rental property.

")